Ceyron, the digital token

hi this time I will discuss about ceyron program which move in financial industry refer to my article below

The progress of the financial industry and the blockchain has now become questionable. For this required token that can combine both. Ceyron Finance Ltd (hereinafter "CFL") intends to bring together the expertise of the financial industry and the revolutionary technology of the blockchain. The CFL disrupts two divergent worlds: cryptocurrency and financial services.

www.ceyron.io will be a cryptocurrency -based investment platform with acryptocurrency trading terminal, debit card capabilities and offer tokens backed by secure credit assets.

The tokens of Ceyron are ...

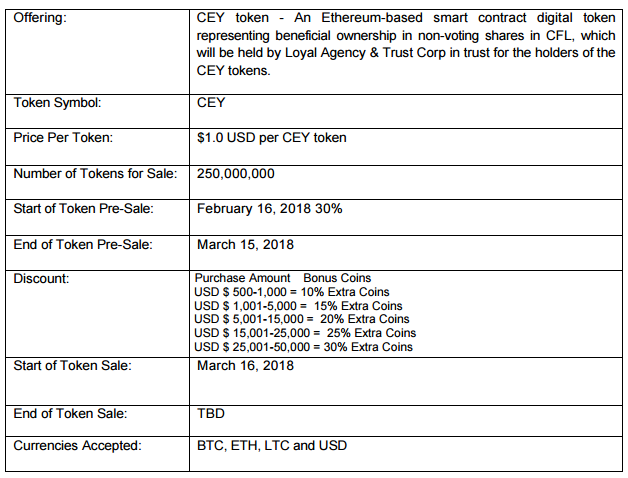

The token is something that can be used instead of money. CEY Tokens are tokens that will be issued to the investor (investors) and that represent beneficial interests in a separate class of non-voting shares of Ceyron. CEY Tokens are smart contracts of functional utility within the Fund. CEY tokens are non-refundable. This is not for speculative investment.

Ceyron Finance Sarl (CFS), is a limited liability company incorporated under the Limited Liability Companies Act (the "Fund") and is wholly owned by Ceyron Finance Ltd. CFL and the Fund have entered into an operating agreement setting out the rights. and the obligations of each party.

The Sub-Fund will be managed and advised by Colombus Investment Management Ltd (the "Fund Manager"). Colombus Investment Management Ltd, is one of the British Virgin Islands registered as an independent alternative investment management company specializing in alternative assets and global asset allocation. The Manager of the Fund will be responsible for the business of the Fund and will perform all services and activities related to the management of the assets, liabilities and operations of the Fund.

Objective and investment strategy

The investment objective of the Fund is to provide attractive returns on invested capital through an exclusive quantitative approach to underwriting credit assets, provided by Colombus Investment Management Ltd. The fund will adhere to an investment strategy based on data science. Nonparametric statistical models are applied to the problem of expected gains in financial investments.

Net income earned by the Fund in a given month is generally reinvested, but a portion of the potential periodic profits may be used to distribute annual dividends to CEY token holders, where such dividends are approved by the board of directors and the voting shareholders of CFL.

Token protected by a credit portfolio for less volatility and more cash flow

The credit asset portfolio will also be secured by a bond to improve stability and returns. The fund manager will use artificial intelligence and machine learning to build a portfolio of secured credit assets.

Blockchain technology provides effective liquidity for investors

Blockchain technology has the potential to provide greater integrity, security, security and transparency. As such, CFL will use the blockchain to ensure the immediate auctioning of low-cost trades in the hope of providing greater liquidity to investors.

Effective prepaid debit cards

Account holders will be able to choose from several cryptocurrencies to use as an offer, and when initiating a transaction (for example, a dinner that costs $ 83.65), the prepaid debit will be used, or The holder can choose a supported cryptocurrency, which will then be sold at the spot price to complete the transaction.

Competitive fees

Since CFL will hold both money and a range of cryptocurrencies at all times, it will be able to facilitate the exchange of funds in cryptocurrency to facilitate transactions and allow CFL to compete with Coinbase for service and fresh.

CFL enters a growing market

The cryptocurrency market grew by more than $ 160 billion ($ 160 billion) last year. Financial giants and central banks have invested in blockchain technology. Large and small investors are looking for a more regulated market that can benefit from the safety nets and insurance coverage offered in any registered security market.

Problem stated for the developing world

The population of the developing world (Southeast Asia, Latin America and Africa) represents more than 2 billion people. Africa alone accounts for 1.2 billion people. It's young and dynamic: 60% are under 50 years old.

Banks are gradually adopting mobile banking to:

1) develop online banking services;

2) provide digital benefits to the parties to integrate millions of people into the formal financial sector;

3) develop merchant payment services.

Low bank rate

According to experts, more than 2.5 billion low-income and / or middle-income people are not tied to a bank. The traditional agency model easily meets the needs of the poorest but no longer fully meets the requirements of banks.

The reasons for the low banking penetration are at two levels .

1. At the client level: most people have only low or very low incomes, and therefore low savings capacity. While the monetization of the economy has increased considerably since the 2000s, the use of a bank is not yet part of spontaneous practices. The emergence and rapid growth of very large microfinance companies is radically changing this situation.

2. At the bank level: excess relative liquidity of banks is not an incentive for customers to develop. Low population density adds average costs to implementing agencies.

Highly competitive market

More than 75% of countries have the majority of services where mobile money services are already available. This increased competition means that consumers have more options. Some subscribe to two or three services simultaneously.

Very low usage rate

Africa is the world leader in the field of mobile money accounts 2% of adults hold a mobile money account in the world, 12% of holders are in Africa. Every year, the number of open mobile money accounts has increased by more than 40% on average. By 2020, the number of Africans with discretionary income - nearly 450 million people - will be comparable to, if not higher than, Western Europe with an average growth rate of 20% per year. By 2020, there will be nearly 800 million people who have a mobile money account. The result: nearly 10 billion transactions per day, valued at nearly 135 billion dollars in 2020.

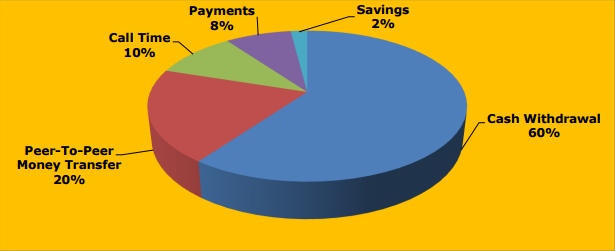

The analysis of the behavior of the average payment user seems to be a general trend: the withdrawal represents at least 60% of the volume of transactions; peer-to-peer transfer operations 20%; purchase of a 10% call time, 8% payments and 2% savings.

A timid pause through the bank card

CEY token holders will have the privilege of receiving their annual dividend on their CFL card.

Lack of secure and unsecured credit for credit applicants

CFL intends to solve the problem in Africa where there is a lack of credit available for most applicants. Specifically, dividends distributed to CEY token holders will allow them to qualify for the credit because dividends could be considered a source of income.

In Africa, there is a lack of stable and sustainable income when it comes to credit applications.

The CFL solution

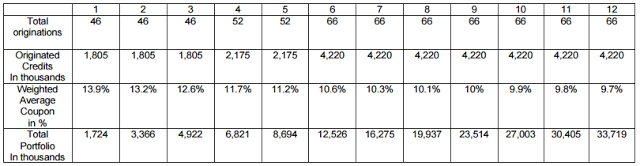

CFL Credit Portfolio

Today, sixty percent (60%) of US mortgages are held by non-banks, up from thirty percent (30%) in 2013. More than four trillion dollars (US $ 4T) in US mortgages are available to select hundreds of bank credit platforms. The fund manager is responsible for approving the solvency and risks associated with the platforms and identifying the credit profiles of the assets issued, the regulatory compliance on the origins, volumes, guarantees, duration and rate, the quality of management and service. The fund manager will be responsible for selecting the best-performing assets available on these platforms for the CFL portfolio, as well as for purging the riskiest assets in the CFL portfolio.

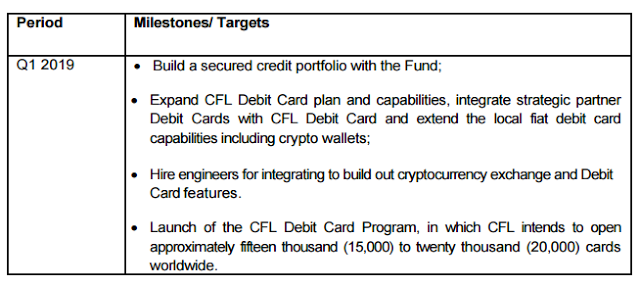

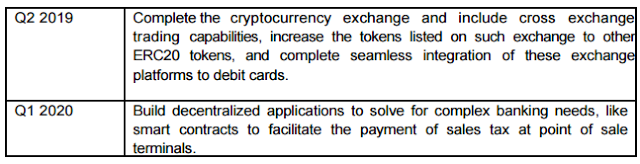

Investment Roadmap

CEY Card

The CEY card will be a physical, virtual and debit MasterCard with mobile application that will allow the use of twenty (20) foreign currencies from a single card. CFL can save up to seventy percent (70%) on these fees. Currency can be traded at both the point of sale (industry average is 3.75% versus 3% for CFL), and also through an app. In addition, unlike the standard one and a half per cent (1.5%) charge for ATM withdrawals, CFL will not charge a fee for ABM withdrawals.The CFL mobile application will contain additional features to transfer funds in any currency between merchants, friends and family accounts, resulting in a zero percent (0%) money transfer fee.

The CFL card plans to have a partner for expense management. This will allow integration from a mobile application to facilitate the management of travel itineraries and links to many travel partners for the management of electronic receipts. In summary, the CFL will be developed to provide increased liquidity in one of the twenty (20) world currencies as well as in major crypto currencies.

LCF and Blockchain

A cryptocurrency (or cryptocurrency) is a digital asset designed to function as a means of exchange that uses cryptography to secure its transactions, to control the creation of additional units and to verify the transfer of assets.

Cryptocurrency has been devised as a method for decentralized transactions with the value held in rare digital assets. This is most striking in societies where governments have lost their money by hyperinflation. Today, fifty percent (50%) of people in the world have bank accounts. In 2014, it was 62%, and cryptocurrencies are taking up more and more space among unbanked people. Cryptocurrency has been devised as a method for decentralized transactions with the value held in rare digital assets. This is most striking in societies where governments have lost their money by hyperinflation. Today, fifty percent (50%) of people in the world have bank accounts. In 2014, it was 62%, and cryptocurrencies are taking up more and more space among unbanked people.

The cryptocurrency currency market has only been operational for a few years. The relatively large differences between Bitcoin's fiat money prices in the different major markets illustrate the current level of maturity of the industry.

Blockchain technology is still young, but it has already proven itself as an immutable registry. Bitcoin is a purely speculative token, and its value, just like diamonds or gold, outside industrial uses, is entirely motivated by the scarcity and the guarantee for the holder that this property is unique and ready to be traded.

CFL Security Token

- CFL intends to provide, but does not guarantee, token holders with an annual dividend, which must be approved by the Board of Directors and holders of voting shares.

- CFL intends to invest eighty-five percent (85%) of the proceeds received by CFL in the Fund, and the Fund will in turn invest in credit assets, seeking to create a stable cash flow. and growing. CEY Token (Cash flow yields can not be guaranteed and may be influenced by market and regulatory conditions)

- CFL intends to use a modest leverage to further enhance the returns on its credit portfolio to facilitate the continued and growing reinvestment of the credit portfolio underlying the CEY tokens (improved returns can not be guaranteed and may be influenced by market and regulatory conditions)

- CFL will enhance its ability to establish its leveraged credit portfolio by providing its warehouse lender with a credit guarantee.

- CFL intends to hold cash, securities and a symbolic reserve at all times to ensure the liquidity of CEY token holders (liquidity of assets can not be guaranteed and may be affected by market and regulatory conditions).

- CFL will enter into alliances with bonding service providers that will be used to mitigate the risk of total capital loss. However, the use of these financial instruments does not constitute a guarantee against any eventuality.

Strategic Alliances

CFL's strategic alliances are established leaders in blockchain technology, finance and banking. CFL intends to enter into a service agreement with Coinfirm.io regarding KYC / AML (Anti Money Laundering) controls for each token holder application. Ambisafe is a pioneer of blockchain technology and ICO offers a company that helps the world become more decentralized since 2010. Their work has been critical on projects such as Tether and Bitfinex. More recently, Ambisafe is behind these successes. Loyal Bank is a bank registered under the laws of Saint Vincent and the Grenadines.

Market plan

The initial offer of CFL coins

The CEY Tokens offer in Saint Vincent and the Grenadines is made under the exemption provided by the Securities Act. The CEY tokens offered herein (and the corresponding non-voting shares of CFL Ltd. held by the nominee) may not be sold to any other bidder in Saint Vincent and the Grenadines unless the provisions of the FSA are respected.

CFL will provide an offering memorandum that will be prepared solely for use by potential CFL investors, to be issued by CFL. The Offering Memorandum will be prepared as part of a private offer to accredited investors, to persons who will be required to verify their accredited investor status by means of a questionnaire and other necessary documents, and other persons responding to participation requirements in the jurisdiction they reside.

Summary of the offer

Technical Offer Mechanism

Potential investors will be asked to provide personally identifiable information when creating an account on ceyron.io to participate in the sale. This information is intended to ensure compliance with the various securities laws of the United States and foreign jurisdictions, as well as customer knowledge (KYC) and anti-money laundering (AML) requirements.

For US investors, they must meet the requirements of the "Qualified Investor" standard under Section 506 (c) of Regulation D of the Securities Act. An investor can demonstrate that he qualifies as a qualified investor by documenting and downloading documents on the ceyron.io website, as described in the following section entitled "Investment Participation".

Participation in the offer

This Offering to prospective investors in the United States is limited to accredited investors as defined in Regulation D of the Securities Act, that is, only those persons or entities that fall into one or more of the following categories:

- Any bank, as defined in subsection 3 (a) (2) of the Securities Act, or any savings and credit association or other institution defined in section 3 (a) (5) (A) of the Securities Act individual or fiduciary capacity; any dealer registered under section 15 of the Exchange Act; any insurance company as defined in section 2 (13) of the Securities Act; any investment company registered under the Investment Companies Act 1940 or a business development corporation within the meaning of section 2 (a) (48) of that Act; any small business investment corporation approved by the United States Small Business Administration under section 301 (c) or (d) of the Small Business Investment Act of 1958; any plan drawn up and maintained by a State, its political subdivisions or any agency or instrument of a State or its political subdivisions for the benefit of its employees, if that plan has total assets in excess of US $ 5 million (5,000,000,000) $);and any benefit plan within the meaning of the Employees Retirement Income Act, 1974, if the investment decision is made by a plan trustee within the meaning of section 3 (21) of that Act, a bank, savings and loan an association, an insurance company or a registered investment advisor, if the total assets of the benefit plan exceed five million US dollars ($ 5,000,000) or, in the case of a self-regulated plan, s);

- Any private enterprise development corporation within the meaning of section 202 (a) (22) of the Investment Advisors Act of 1940;

- Any organization described in section 501 (c) (3) of the Internal Revenue Code of 1986, as amended, any corporation, Massachusetts or a similar trust, or an enterprise, not formed for the specific purpose of acquiring the shares ordinary, with total assets exceeding USD 5 million (USD 5,000,000);

- Any director or officer of the Company;

- Any individual whose individual net worth or net worth together with the spouse of that person, excluding the value of their principal residence net of any mortgage debt and other liens, at the time of purchase exceeds one million USD (1,000,000 $);

- Any individual whose individual income exceeds two hundred thousand US dollars ($ 200,000), or a joint income with his spouse greater than three hundred thousand dollars ($ 300,000), for each of the two most recent years and which reasonably expects to achieve the same level of income for the current year;

- Any trust whose total assets are greater than five million US dollars ($ 5,000,000) and which is not formed for the specific purpose of acquiring common shares that are purchased by a sophisticated person described in Rule 506 (b) (2) (ii) of Regulation D; or

- Any entity whose shareholders are all qualified investors

To invest in this Offer, investors must first create an account and register on www.ceyron.io. In accordance with section 506 (c) of the Securities Act, proof of accreditation status is required to invest. This can be satisfied during the account creation process by completing the accreditation process in one of three ways:

- Accreditation based on the investor's income

- Accreditation based on the net assets of the investor

- Third Party Verification Letter

Post requirements and transfer restrictions

CEY tokens are offered and issued to persons other than United States persons under Regulation S of the Securities Act. Each CEY token subscriber will be deemed to represent, guarantee and accept as follows:

- Either it is: a "Qualified Investor" (as defined in Rule 501 of Regulation D under the Securities Act); or not a "US Person" and acquires the CEY tokens in an "offshore transaction"

- If the subscriber is a purchaser in a transaction in the United States, you acknowledge that until the end of the lock-up period, you will not be authorized to offer, sell or transfer the CEY tokens and after that date, You will no longer be authorized to sell or transfer CEY tokens to any other person in the United States unless they sell all of their CEY tokens to one person in the United States.

- If the Subscriber is a purchaser in a transaction outside the United States within the meaning of Rule S, you acknowledge that you may not sell or transfer the CEY Tokens at any time to any US Person or the account or benefit of 'a US Person within the meaning of Rule 902 under the Securities Act. However, a non-US person may sell CEY tokens to other foreign investors in connection with a foreign operation in accordance with Rules 903 and 904 of the Securities Act and subject to compliance with applicable laws. other territories.

- CEY Tokens will not be sold to anyone under any other offer in Saint Vincent and the Grenadines unless the FSA provisions are followed.

- The Subscriber acknowledges that CFL will not be required to accept the registration of the transfer of CEY Tokens acquired by CFL, except upon presentation of satisfactory evidence to CFL that the restrictions set forth herein have been complied with.

Reporting and transparency for investors

Statement of Net Asset Value of the Fund

CFL intends to publish the net asset value of the Fund on a monthly and quarterly basis on its website.

Methodology for calculating the net asset value

NAV = (accumulated accrued interest - accumulated net loss) / (total outstanding principal + total cash)

The net asset value per CEY token will be calculated by dividing the net asset value by the number of CEY tokens outstanding at the calculation date rounded to the nearest cent. The number of CEY tokens in circulation is calculated as the total number of CEY Tokens issued and outstanding, less any redemptions made by CFL.

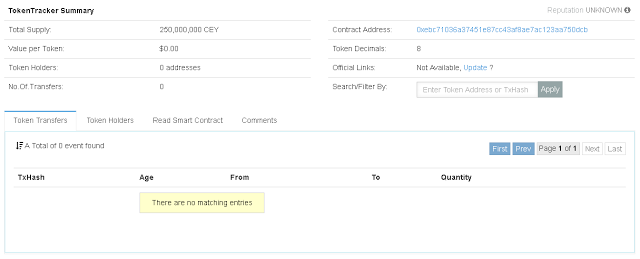

Token of Ceyron

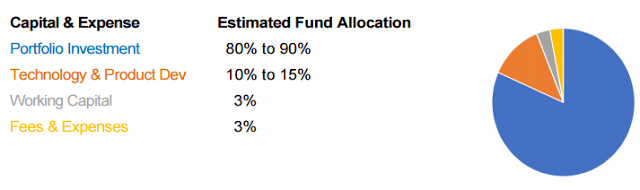

Use of the product

The CEY token funds will be used to finance:

RISK FACTORS

General business risks

In the event of an economic downturn, the company's business plan, ability to generate revenue and overall solvency could be at risk. Companies in the start-up phase in general are very risky and the probability of a failure of the company regardless of the general business climate is possible.

Specific business risks

Investments in vehicles of this nature involve various inherent risks, which may result in: (i) a complete loss of investor capital, (ii) investment results below target, or (iii) lower than expected liquidity, between other.

Credit risk

There can be no assurance that the investment objective of the Fund will be achieved and that investors will not suffer losses. To mitigate the risk of significant credit losses, CFL will take appropriate credit loss provisions, which will be accumulated on each asset in accordance with our credit guidelines, which is typical financial institutions investing in similar credit assets. .

Portfolio risks

There is a risk that CFL will not achieve the intended results. The coupon and the yield to maturity of the CFL Portfolio are critical to our ability to generate consistent dividend for tokenholders and to continue to reinvest in our portfolio, thereby increasing the lasting value of the portfolio and token.

CFL may not be able to achieve the desired level of debt on its portfolio at the desired cost of debt. As a result, there is a risk that the net portfolio return of investors will not be achieved. To the extent that CFL intends to use senior financial leverage, the risk to the investor may be increased by the existence of a senior secured priority lien on the assets in the portfolio.

Token liquidity risk

The CEY Token may not achieve the desired liquidity levels, which would result in less liquidity than expected for investors.

Regulatory risk

CFL's failure to obtain prior regulatory approval in a jurisdiction where it has operated or a regulator's refusal to grant such authorization in a jurisdiction where it could operate could prevent CFL from maintaining or expanding his activities. In addition, changes to laws or regulations, including the adoption of new regulatory licensing, advertising, Internet or e-commerce requirements (or changes to the application or interpretation of regulations existing laws or laws). The jurisdiction in which CFL currently operates may require CFL to cease operations or change the way in which it operates in that jurisdiction. Such changes could also have a material adverse effect on operations, financial condition,

Data privacy and security

All data that is provided to us is stored in a secure computing environment protected by secure firewalls to prevent unauthorized access. The company controls access so that only those who need access to the investor's data have access to it. All members of the CFL team undergo security training and are required to adhere to a comprehensive set of security policies, procedures and standards related to their duties.

CFL Management Team

advisor

Direction

Website: https://ceyron.io/

White Paper: https://ceyron.io/wp-content/uploads/2018/02/White-Paper-ICO-CEY-Token-UPDATED31012018.pdf

author:salsa24

Tidak ada komentar:

Posting Komentar